Hi, I’m Jeremy Eveland. I’m an estate planning attorney. I am licensed in Utah, California, Nevada, and Texas. I help families do estate planning when they are on their second marriage. If you need help, call me at (801) 613-1472 to see if we’d be a good fit to work together.

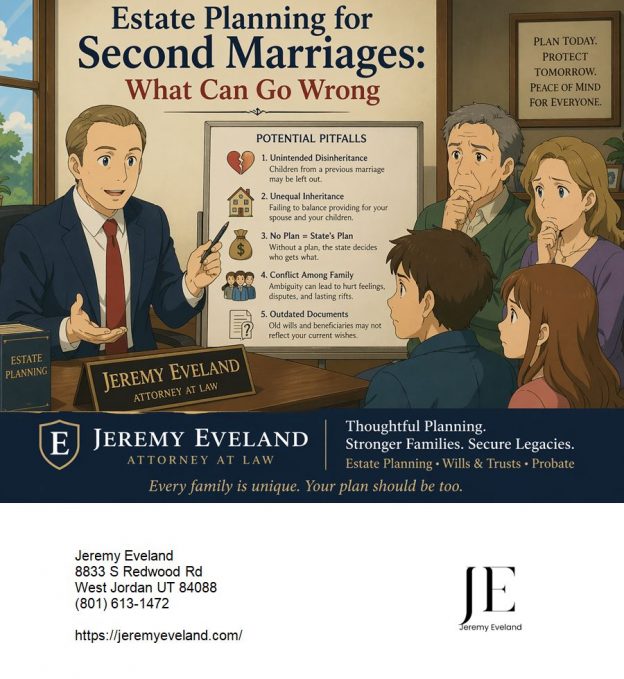

Estate Planning for Second Marriages: What Can Go Wrong

Understanding Second Marriages What Can Go

This guide covers Second Marriages What Can Go and what you need to know. Estate planning for second marriages is fundamentally different from planning for a first marriage because you are usually balancing competing obligations: protecting a current spouse while also preserving inheritances for children from a prior relationship. In Utah, standard estate plans often fail to account for blended-family realities, beneficiary designations, spousal rights, long-term care costs, and what happens after the surviving spouse dies. The result can be exactly the opposite of what the family intended: disinherited children, unintended gifts to a former spouse, court fights between stepchildren and a surviving spouse, and assets consumed by avoidable expenses or Medicaid planning mistakes. Utah’s elective share rules and revocation-on-divorce statute make the details even more important, because some assumptions people make about wills, trusts, and beneficiary forms are simply wrong. The good news is that most of these problems can be prevented with careful planning, updated documents, and the right trust structure. For anyone in a second marriage or blended family, working with an experienced Utah estate planning attorney is critical to make sure the plan actually protects the people you care about most.^1^3

Why second marriages are different

Second marriages create legal and emotional complexity that first-marriage plans often do not handle well. A person may want to provide for a spouse, protect children from a prior marriage, preserve separate property, and avoid family conflict, all at the same time. Utah’s default inheritance rules do not automatically reflect those nuanced goals, especially when children are not mutual to both spouses. In practice, a plan that worked fine in a first marriage often becomes a poor fit once the family structure changes.^4

Utah is not a community property state, but that does not mean all property is automatically separate in a way that solves blended-family problems. Utah uses equitable distribution in divorce, which means marital property is divided fairly under the law, not necessarily equally or according to a family’s informal expectations. That distinction matters because remarriage can blur the line between premarital property, marital property, inherited assets, and jointly titled accounts. A second marriage also often brings emotionally charged decisions about children, stepchildren, the family home, and sentimental items, so planning is rarely just a legal exercise.^6

Real-world problems often start when someone assumes, “My spouse will get everything, and then the kids will get what’s left.” That plan can fail because the surviving spouse may have full legal control over assets received outright, may change their own estate plan, may remarry, or may spend down the estate during life. Another common failure is relying on an old will or trust prepared during the first marriage, which may still name the former spouse, reflect the wrong children, or conflict with current beneficiary forms.^2

Biggest mistakes in second marriages

Failing to update your estate plan after remarriage

One of the most common second marriage estate plan mistakes is simply leaving the old plan in place. A will, trust, power of attorney, and healthcare directive created during a first marriage may still reflect the former spouse’s role or the old family structure. Utah’s revocation-on-divorce statute helps in some situations, but it is not a substitute for a full review after remarriage. It does not fix every problem, especially when assets pass by beneficiary designation or when the estate plan needs to be redesigned for a blended family.^3

The consequence is usually unintended transfer of assets, confusion about fiduciaries, and avoidable disputes. A former spouse may still be named on insurance, retirement, or transfer-on-death forms, and an outdated document may send assets to the wrong person. The safest approach is to review every estate planning document and every beneficiary designation immediately after remarriage, then coordinate them as one plan.^8

Accidentally disinheriting children from a prior marriage

This happens when a person leaves everything to a new spouse with the informal understanding that the surviving spouse will “do the right thing” later for the children. The problem is that once assets are left outright to the spouse, those assets usually become that spouse’s property with no legal duty to preserve them for stepchildren or children from the first marriage. That can be especially painful if the surviving spouse later remarries, changes their will, or simply spends the assets for their own needs.^1

Utah’s elective share law also matters here because a surviving spouse may have statutory rights that override an estate plan that tries to exclude them entirely. In a blended family, the goal is usually not to cut out the spouse, but to balance the spouse’s needs with the children’s inheritance rights. Trusts, specific gifts, and carefully drafted beneficiary structures are usually the tools that make that balance possible.^9

Relying on a simple will instead of a trust

A basic will is often not enough for a blended family because it only controls probate assets and only speaks at death. It does not solve the “second death” problem, and it does not prevent a surviving spouse from changing their own plan after inheriting assets outright. If the plan says “everything to my spouse, then to my kids,” that language often fails in practice because the spouse legally owns what they receive and may owe nothing to stepchildren.^5

A revocable living trust can create far better structure because it can hold assets, control distributions, and define what happens for both spouses and children. In some families, a QTIP trust or bypass trust may be better suited than a simple outright gift. The right answer depends on whether the priority is flexibility, tax planning, creditor protection, or preserving a specific inheritance for children.^1

Ignoring prenuptial or postnuptial agreements

Without a marital agreement, Utah default law may control property rights in a way that does not reflect the couple’s actual intentions. Prenuptial and postnuptial agreements can define separate property, waive or modify rights, and coordinate with an estate plan so the documents work together instead of fighting each other. Many people think prenups are only for the wealthy, but in second marriages they often serve a practical family-protection function.^10

The real risk of skipping this step is that later disputes will be fought under default rules rather than the couple’s own written agreement. That can create uncertainty about what belongs to whom, especially when one spouse brought substantially more assets into the marriage or wants to preserve inheritances for children. A properly drafted agreement can reduce conflict and make the estate plan much more durable. This can solve problems with Estate Planning For Second Marriages.^12

Failing to coordinate beneficiary designations

Beneficiary forms for life insurance, 401(k)s, IRAs, and bank accounts often override a will. That means a perfectly drafted estate plan can be undone by a forgotten form that still names a former spouse, an adult child who should not receive the whole account, or a beneficiary who no longer matches the family’s goals. In Utah, divorce can affect some beneficiary rights by statute, but remarriage does not automatically fix outdated designations.^7^8

Retirement plans can also be subject to spousal consent rules, particularly for certain employer-sponsored plans governed by federal law. That makes it even more important to review each account separately rather than assuming one change updates everything. The practical solution is a full beneficiary audit after remarriage and again after every major life event.^13

Not planning for the surviving spouse’s second death

This is the classic “second death” problem. A spouse dies first, leaves assets to the surviving spouse, and everyone assumes the children will eventually inherit what remains. But the surviving spouse may legally spend, gift, remarry, or redirect those assets through a new plan. By the time the surviving spouse dies, the original spouse’s children may inherit far less than expected, or nothing at all.^4

Trust structures are the usual fix because they can let the surviving spouse benefit during life while preserving the remainder for children. QTIP trusts, bypass trusts, and other carefully drafted arrangements can define the surviving spouse’s rights while limiting what happens to the principal at death. The specific tool depends on the family’s goals and tax profile.^1

Allowing disputes between spouse and stepchildren

When it comes to Estate Planning For Second Marriages, blended families are especially vulnerable to litigation because the emotional stakes are so high. Family members may accuse each other of undue influence, hidden transfers, or favoritism, especially when the surviving spouse controls finances or when one child is named trustee or personal representative. The family home and sentimental property often become flashpoints for these conflicts.^9

These disputes are expensive and deeply damaging because they can freeze assets, delay administration, and permanently fracture relationships. Clear documents, documented decision-making, mediation provisions, and neutral fiduciaries reduce the chance that a grieving family turns into a courtroom battle. Sometimes the best planning decision is not just what the documents say, but who is entrusted to carry them out.^9

Overlooking long-term care and Medicaid planning

Long-term care can wipe out a blended family estate faster than almost anything else. If one spouse needs extended nursing home care, the cost can consume assets that the couple intended to leave to children from a prior marriage. Medicaid rules and spend-down requirements can further complicate matters if the family has not planned ahead.^9

The risk is especially serious where one spouse is far more likely to need care or where most of the estate is tied up in illiquid assets such as a home or family business. A blended-family plan should consider insurance, asset protection strategies, and how care costs will be paid without destroying the inheritance structure. This is one area where estate planning and elder law should work together.^9

Failing to address the family home

The family home often carries both emotional and financial value, which is why it causes so many problems. Without a clear plan, the surviving spouse may want to stay in the home while the children want to sell it or protect their remainder interest. Joint tenancy, life estates, and trust ownership each handle this differently, and each has tradeoffs.^15

A well-drafted plan should spell out who may live in the home, who pays taxes and upkeep, whether the property can be sold, and how sale proceeds are distributed. If the house is a major asset, it should not be left to assumptions. The home should be addressed in writing with the same care as cash or investments.^15

Not communicating the plan

Many estate fights begin with surprise. If stepchildren do not understand the plan, they may assume they were cut out intentionally. If the surviving spouse does not understand their rights, they may feel deceived or pressured. Silence often creates more conflict than the plan itself.^1

Open communication does not mean disclosing every private detail, but it does mean setting expectations and reducing the chance of shock. In many families, the most effective discussions happen with the attorney present, so the legal reasoning is clear and the emotional temperature stays manageable. That approach can save years of resentment later.^1

Real cost of mistakes

When estate planning goes wrong in a second marriage, the losses are usually larger than people expect. Financially, families can spend heavily on litigation, court filings, expert witnesses, and administration delays, while also losing assets to care costs or poor structure. Tax inefficiency can also increase the damage if the plan does not use available exemptions or trust design properly.^9

The time cost can be severe as well. Probate disputes, will contests, trust disputes, and spousal-rights litigation can take months or years, during which assets may be frozen or poorly managed. That delay creates added stress just when the family is already grieving.^1

The emotional cost is often the worst part. Children may become estranged from a surviving spouse, siblings may stop speaking to one another, and the family may be left with a permanent sense that the decedent’s wishes were never truly honored. Most of those outcomes are preventable with careful planning and honest communication.^9

Tools that help

Revocable living trusts

A revocable living trust is often the backbone of a blended-family estate plan because it allows the owner to control assets during life and direct them at death without relying entirely on probate. It can be written to provide income or housing for a surviving spouse while protecting principal for children later. It is flexible, and it can be updated as family circumstances change.^16

Its limitation is that it only works if assets are actually transferred into the trust and maintained properly. It also requires careful drafting so the surviving spouse has enough support without giving away the children’s inheritance. A trust is powerful, but it is only as good as the design behind it.^16

QTIP trusts

A QTIP trust is especially useful when someone wants to provide for a surviving spouse but ultimately preserve the remaining assets for children from a prior marriage. The surviving spouse can receive income or use of trust assets, while the remainder passes to the named children at the second death. This structure can be a strong fit for estate planning second marriage Utah situations.^1

Its limitation is reduced flexibility. The surviving spouse usually cannot redirect the remainder to a new family or rewrite the ultimate beneficiaries, which is exactly the point. It is best used when preserving a specific inheritance is more important than giving the surviving spouse complete control.^1

Bypass trusts

Bypass or credit shelter trusts may help maximize estate tax exemptions and protect assets for children. They are often used in more complex estates where tax exposure and multigenerational planning matter. For blended families, these trusts can also create a cleaner separation between what benefits the surviving spouse and what ultimately belongs to the children.^1

Their limitation is complexity. They require careful drafting, funding, and administration, and they are not necessary for every family. Whether they make sense depends on asset levels, tax concerns, and the family’s distribution goals.^1

Life estate deeds

A life estate can allow a surviving spouse to remain in the home for life or for a defined period while ensuring the property passes to children later. This may be useful when the house is the main asset and both housing stability and inheritance protection matter. It creates a clear housing right without giving outright ownership.^15

The downside is that life estates can be rigid, hard to unwind, and sometimes difficult to coordinate with taxes, maintenance, and sale decisions. They are best used when the family truly wants a defined occupancy arrangement rather than a flexible ownership structure.^15

Prenuptial and postnuptial agreements

These agreements are a major tool for coordinating marital rights with estate planning goals. They can protect premarital assets, define inheritance expectations, and make the estate plan easier to enforce later. In second marriages, they often prevent disagreement before it starts.^11

Their limitation is that they must be drafted carefully and comply with Utah law. They should also be consistent with wills, trusts, deeds, and beneficiary forms, because conflicting documents create confusion and litigation risk.^12

ILITs

An irrevocable life insurance trust can provide liquidity outside the taxable estate and can be directed to specific beneficiaries. That can be very helpful in a blended family where cash is needed to balance unequal inheritances, pay taxes, or provide funds to children without giving the surviving spouse control over the proceeds.^1

The limitation is that an ILIT is generally irrevocable, so it is less flexible than a revocable trust. It should be used when long-term control and tax efficiency are more important than easy modification.^1

Beneficiary designations and TOD/POD accounts

Non-probate transfers are often the fastest way assets pass, which makes them powerful and dangerous. If they are not aligned with the estate plan, they can override the careful trust structure you created. After remarriage, every life insurance policy, retirement account, bank account, and transfer-on-death registration should be reviewed together.^3^7

These tools are simple but not self-correcting. If a beneficiary form is wrong, the account may pass wrong even if the will is perfect. That is why beneficiary audits are an essential part of blended-family planning.^8

Powers of attorney and healthcare directives

In a second marriage, naming the right decision-maker matters as much as naming the right beneficiary. Powers of attorney and healthcare directives should reflect who is trusted to handle finances and medical choices if incapacity strikes. In some families, that person is the spouse; in others, it may be an adult child or another neutral person.^16

Their limitation is that they do not control inheritance at death. They are critical for incapacity planning, but they must work alongside the rest of the estate plan rather than replace it.^16

How an attorney helps

An experienced Utah estate planning attorney does more than draft documents. The attorney should analyze the family dynamics, identify competing goals, and design a plan that addresses the spouse, children, stepchildren, property titles, and beneficiary designations as one integrated system. That coordination is usually where blended families succeed or fail.^11

An attorney can also help draft trusts that preserve inheritance while still supporting the surviving spouse. That may include building in trustee discretion, health and maintenance standards, housing rights, or distribution schedules that fit the family. For higher-value estates, the attorney can also address tax exposure and creditor-risk concerns.^1

A good planner also helps manage expectations. That may mean family meetings, written explanations, and making sure everyone understands why the plan is structured the way it is. When the family understands the plan, there is less room for suspicion later.^1

What to do now

- Review and update any estate plan from your prior marriage.

- Audit all beneficiary designations on insurance, retirement accounts, and bank accounts.

- Talk openly with your spouse about goals, concerns, and expectations.

- Consider a prenuptial or postnuptial agreement if property rights need clarity.

- Meet with a Utah estate planning attorney who regularly handles blended families.

- Decide whether a trust is appropriate for your family structure.

- Address the family home, personal property, and sentimental items specifically.

- Plan for incapacity and long-term care before a crisis happens.

- Explain the plan to children and stepchildren at a level that reduces surprises.

- Review the plan every three to five years or after a major life event.^11^1

Common mistakes

- Assuming a will alone is enough to protect children from a prior marriage.

- Relying on a spouse’s verbal promise instead of legal documents.

- Forgetting to update beneficiary designations after remarriage.

- Leaving everything outright to a surviving spouse with no safeguards.

- Ignoring Utah elective share rights.

- Underestimating Medicaid and long-term care costs.

- Commingling separate property with marital property.

- Forgetting digital assets, business interests, or inherited real estate.

- Treating estate planning as a one-time event instead of an ongoing process.^3^1

FAQ

What makes estate planning for second marriages different?

It requires balancing the needs of a current spouse with the rights of children from prior relationships. The legal documents must reflect that balance clearly, or the plan can fail.^4

Can my spouse inherit everything if I die without a will in Utah?

Not necessarily. Utah intestacy law gives a surviving spouse different shares depending on whether there are children from a prior relationship.^5

What is Utah’s elective share and how does it affect my estate plan?

The elective share gives a surviving spouse a statutory right to claim part of the augmented estate, even if the will says otherwise. That means a plan cannot ignore spousal rights without careful drafting.^17

Do I need a prenuptial agreement if I’m remarrying?

It is often strongly worth considering, especially when you want to preserve separate property or protect children from a prior marriage. A prenup can coordinate property rights with your estate plan.^12

What happens to my children’s inheritance if I remarry?

Without a well-designed plan, some or all of it may go to your new spouse first and be controlled by that spouse later. A trust can preserve inheritance rights while still supporting the spouse.^4

Can my new spouse change my estate plan after I die?

Not your plan, but they may have legal control over assets they inherit outright and can make their own estate choices. That is why leaving assets outright can be risky in blended families.^4

What is a QTIP trust and how does it protect my children?

A QTIP trust can support a surviving spouse during life while preserving the remainder for your children after the spouse dies. It is a common solution for blended families.^1

Should I put my house in a trust if I’m in a second marriage?

Often yes, if you want to control who can live there, who pays expenses, and who receives it later. The right structure depends on your goals and whether you want flexibility or certainty.^15

Do beneficiary designations override my will in Utah?

Yes, for many assets they do. Life insurance, retirement accounts, and POD/TOD accounts often pass by beneficiary form rather than by will.^7

What happens to my retirement accounts when I remarry?

You should review the beneficiary forms immediately because the retirement account may pass to whoever is named there, subject to plan rules and possible spousal-consent requirements.^14

Can my stepchildren inherit from me automatically?

No. Stepchildren generally do not inherit automatically unless you specifically provide for them in your estate plan or leave them something by beneficiary designation or trust.^4

What is the difference between a revocable and irrevocable trust?

A revocable trust can usually be changed during life, while an irrevocable trust generally cannot be easily changed. Revocable trusts offer flexibility; irrevocable trusts offer more control and sometimes tax or asset-protection benefits.^16

How do I protect assets I brought into a second marriage?

Use clear title, a marital agreement if needed, and an estate plan that keeps those assets separate or directs them through trust structures. Commingling can make protection harder.^6

What if my spouse and children from a prior marriage don’t get along?

That is exactly when clear planning matters most. Trusts, neutral fiduciaries, and detailed written instructions can reduce conflict.^9

Can I disinherit my spouse in Utah?

Not completely without consequence. Utah law gives a surviving spouse rights that may include an elective share unless waived or properly addressed.^17

What are the tax implications of estate planning in a second marriage?

They depend on asset level, trust design, and whether the plan is intended to preserve exemptions for children while supporting a spouse. Complex estates should be reviewed with tax-aware planning.^1

How do I handle life insurance in a blended family estate plan?

Life insurance can be used to equalize inheritances or provide liquidity outside probate. The beneficiary designation must match the overall plan.^8

What happens if I don’t update my estate plan after remarriage?

Old documents, old beneficiary forms, and old assumptions can control the outcome. That often produces unintended transfers and disputes.^2

How often should I update my estate plan?

Every three to five years is a good rule of thumb, and immediately after major life events such as marriage, divorce, birth, death, significant asset changes, or a move.^2

What is a life estate and when should I use one?

A life estate lets one person live in or use the property for life, after which it passes to someone else. It can work well for home protection but may be too rigid for some families.^15

Can a will be contested by stepchildren in Utah?

Yes. Stepchildren may challenge a will or trust on grounds such as undue influence, lack of capacity, or improper execution.^18

What is an irrevocable life insurance trust?

An ILIT owns a life insurance policy and directs proceeds according to the trust terms. It can provide liquidity and control for children or other beneficiaries.^1

How does Medicaid planning affect my estate plan in a second marriage?

Long-term care costs can deplete assets intended for children, so Medicaid and care planning should be part of the broader estate strategy.^9

What should I do first when planning my estate after remarriage?

Start with a complete review of your existing documents, beneficiary forms, property titles, and family goals. Then build the new plan around those facts.^3

How do I choose the right estate planning attorney for a blended family?

Choose a Utah estate planning attorney who regularly handles blended-family planning, trusts, prenuptial agreements, probate, and family-law overlap. Experience with both estate planning and family dynamics matters.^11

Utah laws that matter

Utah’s elective share statute gives a surviving spouse statutory rights that can affect how much of an estate can be redirected away from them. That is one reason a second-marriage plan needs careful drafting instead of informal promises.^17

Utah’s revocation-on-divorce rules can affect wills and some nonprobate transfers, but they are not a complete replacement for an updated plan after remarriage. Utah’s code also addresses how divorce affects certain beneficiary designations and other transfers.^2^3

Utah’s probate and trust rules, along with its will-execution requirements, also matter because a document that is invalidly signed or poorly coordinated can fail when it is needed most. Premarital agreements must also satisfy Utah’s formal requirements, including being in writing and signed.^19

Next Steps

Estate planning for second marriages goes wrong when people rely on assumptions instead of legal structure. The most common failures are outdated documents, beneficiary-designation mistakes, outright gifts to a surviving spouse with no protection for children, and no plan for the home, long-term care, or the surviving spouse’s second death. Fortunately, almost all of these problems are avoidable with the right documents and regular reviews.^8^1

If you are entering a second marriage, currently in one, or helping a loved one navigate a blended family, the smartest move is to get individualized legal guidance early. Utah Estate Planning Attorney Jeremy Eveland provides estate planning, trust creation, prenuptial agreements, probate administration, and blended family legal services.^11

^20^22^24^26^28^30^32^34^36^38^40^42

Jeremy Eveland

17 North State Street

Lindon UT 84042

(801) 613-1472

For legal assistance regarding Second Marriages What Can Go, contact Jeremy Eveland. We handle Second Marriages What Can Go cases and provide guidance on Second Marriages What Can Go for clients.

For legal assistance regarding Second Marriages What Can Go, contact Jeremy Eveland. We handle Second Marriages What Can Go cases and provide guidance on Second Marriages What Can Go for clients.

For legal assistance regarding Second Marriages What Can Go, contact Jeremy Eveland. We handle Second Marriages What Can Go cases and provide guidance on Second Marriages What Can Go for clients.

For legal assistance regarding Second Marriages What Can Go, contact Jeremy Eveland. We handle Second Marriages What Can Go cases and provide guidance on Second Marriages What Can Go for clients.

For legal assistance regarding Second Marriages What Can Go, contact Jeremy Eveland. We handle Second Marriages What Can Go cases and provide guidance on Second Marriages What Can Go for clients.

For legal assistance regarding Second Marriages What Can Go, contact Jeremy Eveland. We handle Second Marriages What Can Go cases and provide guidance on Second Marriages What Can Go for clients.

For legal assistance regarding Second Marriages What Can Go, contact Jeremy Eveland. We handle Second Marriages What Can Go cases and provide guidance on Second Marriages What Can Go for clients.

For legal assistance regarding Second Marriages What Can Go, contact Jeremy Eveland. We handle Second Marriages What Can Go cases and provide guidance on Second Marriages What Can Go for clients.