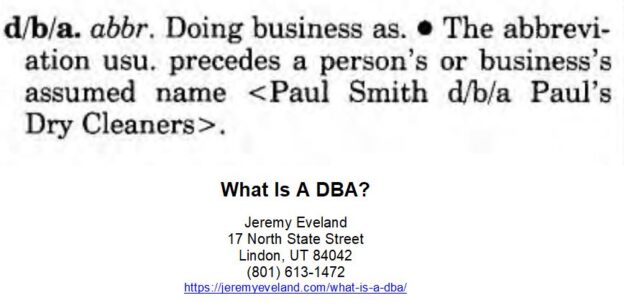

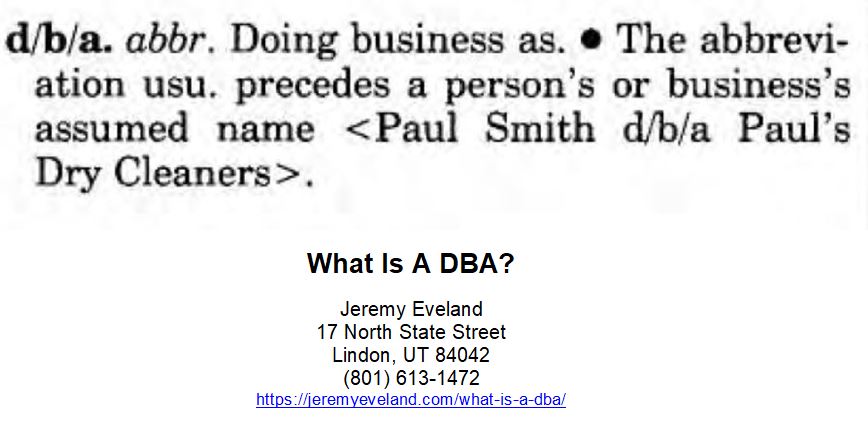

A DBA, or Doing Business As, is a type of business structure that allows an individual or company to operate under a name that is different from their legal name. A DBA is also sometimes referred to as an alias, assumed name, fictitious business name, or trade name. For example, a business owner operating under their own name might file a DBA to do business as “ABC Widgets,” rather than their own name.

When registering a DBA, the business owner is usually required to submit a form to the county or state in which they are doing business. This form typically includes the name of the business, the address of the business, and the name and address of the business owner. Depending on the state, the owner may also be required to publish a notice in a local newspaper or other periodical, alerting the public of the DBA registration.

In most cases, a DBA does not provide the same legal protections as a corporation or limited liability company (LLC). Without registering as a separate business entity, the business owner remains personally liable for any debts and obligations associated with the business. A DBA also does not offer the same tax advantages, as the business is still taxed as a sole proprietorship or partnership

Business Structures in Utah

Business structure is a vital component of any successful organization. It is the way in which the business is set up and maintained, and it can have a significant effect on the company’s ability to operate effectively. In Utah, there are a variety of different business structures available, including sole proprietorships, limited liability companies (LLCs), corporations, and partnerships. Each of these structures offer different levels of protection and exposure to the owners and their businesses.

For example, a sole proprietorship is the simplest type of business structure. This is when one individual owns the business and is solely responsible for its operations. The owner may operate the business under their own name, or they may register a “doing business as” (DBA) name with the state. This DBA name must be unique and should be registered in the state’s database of business names. This will provide a degree of protection for the owner and their business from liability and taxation.

A limited liability company (LLC) is a more complex type of business structure. LLCs are popular in Utah due to their high degree of protection and flexibility when it comes to business operations. LLCs have a number of advantages, including limited liability protection for the owners, reduced filing fees, and the ability to manage the business in a way that suits the owners’ needs. In addition, LLCs provide tax and accounting benefits, such as the ability to pass tax credits onto their owners.

Partnerships are another popular business structure in Utah. This type of business structure is similar to a sole proprietorship in that two or more individuals own the business. However, partnerships offer the advantage of having two or more owners to share the risk of running the business. Partnerships also offer tax advantages, such as the ability to pass profits and losses onto the partners.

Finally, corporations are the most complex type of business structure. Corporations are owned by shareholders and managed by a board of directors. Corporations offer a number of advantages, including limited liability protection for the owners and the ability to raise capital through the sale of stock. However, corporations are subject to a number of regulations and taxes, so it is important to consider all of the options before making a decision.

No matter which type of business structure you choose, it is important to have a clear understanding of the regulations and laws that apply to your business. In Utah, the Division of Corporations and Commercial Code Administration is responsible for registering and managing businesses. It is also important to consider the fees associated with each type of business structure, as well as the time and energy it will take to set up the business. With careful thought and planning, however, the right business structure can provide a strong foundation for success.

Business Formation

Business formation is a critical step for entrepreneurs seeking to establish a business and start generating revenue. In Utah, business formation is typically accomplished by registering a dba name, sole proprietorship, legal name, business name, legal entity, or fictitious name. A dba name is a different name used by an individual or business to identify itself to the public, while a sole proprietorship is a business structure that is owned and operated by a single business owner. For a dba registration, business owners must file an application with their county clerk. Additionally, many states require a business owner to register a fictitious business name with the state.

When forming a sole proprietorship, a business owner typically uses his or her own name as the business name. In some cases, business owners may register a “trade name” which is a name other than their own personal name. This allows them to use a different name for the business that is more descriptive or easier to remember. In addition, many states require business owners to register a dba degree, which is an additional designation that they can use to identify the business.

When forming a legal entity, such as a general partnership or limited liability company, business owners must appoint a business administration to handle business affairs. This includes opening a business bank account, obtaining necessary permits and licenses, and filing all required paperwork with the state. Depending on the business structure, the business owners may be personally liable for any debts or obligations of the business. Therefore, it is important for business owners to understand the legal protections of the particular business structure they choose.

Noise levels and personal assets are two important considerations when selecting a business structure. For example, a sole proprietorship provides the greatest amount of legal protection for the business owner’s personal assets, but there is no limit on the amount of noise associated with the business. On the other hand, a limited liability company offers more legal protections for the business owner’s personal assets, but it also limits the amount of noise generated by the business.

The cost of business formation also varies depending on the type of business structure chosen. For example, the cost of filing a fictitious business name is typically lower than the cost of registering a dba or forming a legal entity such as a general partnership or limited liability company. Additionally, the state fees associated with forming a business may vary from state to state.

In conclusion, business formation is a critical step for entrepreneurs looking to launch a business. There are a variety of factors to consider, including the type of business structure selected, the cost associated with filing a fictitious business name or dba degree, and the legal protections of the particular business structure chosen. Additionally, many states require business owners to register a fictitious business name with the state. It is important for entrepreneurs to understand all of the options available to them when forming a business in order to ensure the most successful business formation.

DBA Lawyer Consultation

When you need legal help from a Business Lawyer about a DBA, call Jeremy D. Eveland, MBA, JD (801) 613-1472 for a consultation.

Jeremy Eveland

17 North State Street

Lindon UT 84042

(801) 613-1472

Millcreek, Utah is home to many businesses and entrepreneurs, and they all need the expertise of a business succession lawyer. A business succession lawyer is a legal professional who specializes in the area of business succession law. This type of law covers a variety of topics, including estate planning, business succession planning, transfer of ownership, asset protection, and taxation. A business succession lawyer in Millcreek, Utah can provide legal advice and services to business owners, entrepreneurs, and families in the area.

“Good things happen to those who hustle.” – Anais Nin

Good things (usually) don’t just fall into your lap, and there’s no use waiting around and hoping they will. Want to start a side hustle? Stop thinking and talking about it. Get started today, good things will happen when you work hard for them—and position yourself to identify which opportunities you can take advantage.

“The dream is free. The hustle is sold separately.”

It doesn’t cost you anything to dream—time, money, or hard work. Hustle, on the other hand, costs all of that.

“I am deliberate and afraid of nothing.” – Audre Lorde

Adopt a deliberate mindset, and do not be afraid to take chances. This motivational quote is a reminder that if you want to be successful, you will need to work like your life (style) depends on it.

“I began to realize how important it was to be an enthusiast in life. If you are interested in something, no matter what it is, go at it full speed ahead. Embrace it with both arms, hug it, love it, and above all become passionate about it. Lukewarm is no good. Hot is no good either. White hot and passionate is the only thing to be.” – Roald Dahl

When in doubt, don’t half-ass it. You can’t afford to.

“Remembering that you are going to die is the best way I know to avoid the trap of thinking you have something to lose. You are already naked. There is no reason not to follow your heart.” – Steve Jobs

It’s a bit nihilistic, but it’s also pretty damn motivating. What do you really have to lose in this life? Failure in business won’t kill you, and you’ll be able to get back into the game if you have the drive. Pick yourself up and hustle again.

Business succession lawyers in Millcreek, Utah can provide legal services to business owners, entrepreneurs, and families in the area. They can provide advice on how to structure a business entity, such as a sole proprietorship, partnership, limited liability company (LLC), or corporation. They can also provide advice on how to draft a valid succession plan, which is the document that will outline the ownership and control of the business. They can also provide advice on how to transfer ownership and control of a business in the event of a death or disability.

“You can’t use up creativity. The more you use, the more you have.” – Maya Angelou

The best way to get your side hustle moving is to flex those creative muscles. No matter how small or seemingly insignificant. The act of exercising your creative muscle will help you perfect your craft and become even better. Create. Create. Create.

“I always did something I was a little not ready to do. I think that’s how you grow. When there’s that moment of, ‘Wow, I’m not really sure I can do this,’ and you push through those moments, that’s when you have a breakthrough.” – Marissa Mayer

Never stop challenging yourself. The day you do, you’re falling behind. Do things you’re a little not-ready-to-do yet. That’s how you grow and have breakthroughs.

“Never let go of that fiery sadness called desire.” – Patti Smith

If you lose your ambition, you’ve lost the drive to succeed. Keep that desire to be something greater burning inside of you, and bookmark this motivational quote—it’ll get you through the tough times that lie ahead.

“Challenges are gifts that force us to search for a new center of gravity. Don’t fight them. Just find a new way to stand.” – Oprah Winfrey

If you feel like your side hustle is hitting a roadblock, reframe it: It’s adjusting its center of gravity. This motivational quote is inspiration to constantly adapt in the face of challenges. Any time you feel procrastination creeping in, strive to be aware of it and treat it like a plague—stop procrastinating the moment you realize you’re doing it and find a reward for completion of the milestone.

“What would you do if you weren’t afraid?” – Sheryl Sandberg

Take a minute to think about that one. If truly nothing was stopping you, nothing in your way, nothing to be afraid of, what would you do? This is an inspiration to do exactly that. Right now. What are you waiting for? Should you quit your job to pursue your side project that’s gaining momentum? Well, maybe. You tell me. What are you afraid of?

“It is not true that people stop pursuing dreams because they grow old. They grow old because they stop pursuing dreams.” – Gabriel García Márquez

Your passion for your dream will keep you young and invigorated. This is a reminder not to fall into the trap of contentment, laziness, or stagnation. Find a business idea that helps you achieve your most meaningful goals in life—and keep pushing towards it until you’re there.

Business succession law is an important area of the law that business owners, entrepreneurs, and families should have a basic understanding of. This type of law deals with the transfer of ownership and control of a business from one generation to the next. This law is especially important for businesses that are structured as partnerships or limited liability companies (LLCs). Business succession law also covers estate planning, which is the legal process of managing and protecting the assets of an individual or family.

“I don’t count my sit-ups; I only start counting when it starts hurting because they’re the only ones that count.” – Muhammad Ali

Going through the routine isn’t good enough, and more importantly, it’s not going to keep pushing you to grow. This is a reminder that the only way to get to the zone where you’re growing, and pushing the limits, is to continue to push yourself beyond your comfort zone.

“One, remember to look up at the stars and not down at your feet. Two, never give up work. Work gives you meaning and purpose and life is empty without it. Three, if you are lucky enough to find love, remember it is there and don’t throw it away.” – Stephen Hawking

“Innovation distinguishes between a leader and a follower.” – Steve Jobs

Are you imitating or innovating? Keep asking yourself that as you pursue your work, and use this motivational quote to push yourself in the right direction and strive to be a leader.

“I have not failed. I’ve just found 10,000 ways that won’t work.” – Thomas Edison

No one has ever done anything important (perfectly) on the first try—failing once or even dozens of times—should never mean failing forever. When you fail with a big project, don’t land a new client you’ve been pitching, under-deliver on the results you were expecting, or get down about a cold email that went unanswered, always limit the amount of time you allow for being discouraged, to no more than an afternoon. After that, it’s time to dust yourself off, figure out where you went wrong, and start hustling again.

“Do not go where the path may lead, go instead where there is no path and leave a trail.” – Ralph Waldo Emerson

It’s easier to follow established career paths and societally acceptable professions, but if that’s not going to make you the happiest version of yourself—then it’s your responsibility to deviate from the path. Welcome to entrepreneurship. Leaders carve out their own path instead of following the masses and you should inspire others to follow you. You can’t expect people to flock to your cause; give them a compelling reason that they won’t be able to ignore you any longer.

“You gotta run more than your mouth to escape the treadmill of mediocrity. A true hustler jogs during the day, and sleepwalks at night.” – Jarod Kintz

Basically, put your money where your mouth is. Don’t just tell everyone about that great idea of your, those dreams of owning your own business—this is a reminder to actually make daily progress towards bringing it to life. Learn the skills you’ll need to excel, take the right online business courses to level up your game, network with the right people, find mentors. Don’t make excuses—hustle hard.

“Lift up the weak; inspire the ignorant. Rescue the failures; encourage the deprived! Live to give. Don’t only hustle for survival. Go, and settle for revival!” – Israelmore Ayivor

If you’re doing what you do for just you, you’re probably doing it wrong. Strive to do better, give back, and inspire others. This is a reminder that there’s plenty of room for generosity in the hustle. And when you do pay it forward, the benefits you will experience come back tenfold.

“Hustle until you no longer need to introduce yourself.” – Anonymous

No one asks Bill Gates who he is, use this to achieve greatness—remind yourself of that and you can’t lose in the long run.

“Things work out best for those who make the best of how things work out.” – John Wooden

Success almost never comes in a neat package. This motivational quote will remind you to make the best of what you have, and what happens even if you fail.

“If you are not willing to risk the usual, you will have to settle for the ordinary.” – Jim Rohn

Mediocre is easy. It takes work to become truly great. Learn to love the hustle. If you want mediocrity, invest in a low risk, low return lifestyle.

You want to fulfill your dreams as an entrepreneur? You’re going to have to hustle a lot.

Business Succession Lawyer Millcreek Utah Consultation

When you need legal help with a business succession in Millcreek Utah, call Jeremy D. Eveland, MBA, JD (801) 613-1472.

Jeremy Eveland

17 North State Street

Lindon UT 84042

(801) 613-1472

For legal assistance regarding Business Succession Lawyer Millcreek Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Millcreek Utah cases and provide guidance on Business Succession Lawyer Millcreek Utah for clients.

For legal assistance regarding Business Succession Lawyer Millcreek Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Millcreek Utah cases and provide guidance on Business Succession Lawyer Millcreek Utah for clients.

For legal assistance regarding Business Succession Lawyer Millcreek Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Millcreek Utah cases and provide guidance on Business Succession Lawyer Millcreek Utah for clients.

For legal assistance regarding Business Succession Lawyer Millcreek Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Millcreek Utah cases and provide guidance on Business Succession Lawyer Millcreek Utah for clients.

For legal assistance regarding Business Succession Lawyer Millcreek Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Millcreek Utah cases and provide guidance on Business Succession Lawyer Millcreek Utah for clients.

For legal assistance regarding Business Succession Lawyer Millcreek Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Millcreek Utah cases and provide guidance on Business Succession Lawyer Millcreek Utah for clients.

For legal assistance regarding Business Succession Lawyer Millcreek Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Millcreek Utah cases and provide guidance on Business Succession Lawyer Millcreek Utah for clients.

For legal assistance regarding Business Succession Lawyer Millcreek Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Millcreek Utah cases and provide guidance on Business Succession Lawyer Millcreek Utah for clients.

If you are on this webpage you probably understand that proper Business Succession Planning is essential and that you need to have a Lehi Utah Lawyer help you to Secure Your Business’s Future. This is part of Business Succession Law and under the main category of Business Law.

Business succession planning is an important factor for any business owner to consider, as it can help to ensure the business’s longevity and success into the future. Succession planning is the process of planning for the transfer of ownership and management of a business from one generation to the next. It is a critical process that should be undertaken to ensure the future of the business and its owners.

Business succession planning involves more than just the transfer of ownership. It also involves the transfer of management, the development of a succession plan, and the implementation of strategies to ensure a successful transition. Proper planning can help to ensure that the business’s future is secure and that it will continue to be successful for years to come.

One of the key elements of business succession planning is the development of a succession plan. A succession plan is a document that outlines the ownership and management of the business and the steps that will be taken to ensure a smooth transition from one generation to the next. The plan should include the names of the designated successors, the timeline for the transition, and the strategies that will be used to ensure a successful transition.

The development of a succession plan should be undertaken with the help of an experienced business succession planning consultant. These consultants have the expertise and knowledge necessary to help business owners develop a plan that is tailored to the needs of their business. Consultants may also be able to provide advice on how to best manage the transition process, as well as provide advice on how to prepare for the future of the business.

In addition to developing a succession plan, business owners should also consider the financial aspects of the transition. This includes making sure that the business is properly insured and that the necessary taxes and fees are paid. It is also important to consider the estate taxes that may be applicable in the event of a business sale or transfer.

The transition process should also be carefully considered. It is important to ensure that the transition is smooth and that the business is not disrupted. The transition process should also involve the transfer of ownership and management of the business, as well as the development of any necessary agreements.

The transition process should also include the development of a buy-sell agreement. This agreement is a legally binding document that outlines the terms and conditions of the sale or transfer of the business. It should include the names of the buyers and sellers, the purchase price, the payment terms, and any other relevant information.

The transition process should also include the consideration of any outside parties that may be involved in the transaction. This may include family members, creditors, or other investors. It is important to ensure that all parties involved in the transaction are aware of the terms and conditions of the buy-sell agreement and that they agree to the terms.

The transition process should also include the consideration of any other related entities. This may include trustees, executors, or other entities. It is important to ensure that all of the relevant entities are aware of the terms and conditions of the buy-sell agreement and that they agree to the terms.

The transition process should also include the consideration of any key employees. These employees may be key to the success of the business and should be taken into account when planning for the transition. It is important to ensure that these employees are aware of the terms of the buy-sell agreement and that they agree to the terms.

The transition process should also include the consideration of any financial life insurance policies that may be necessary. These policies can help to protect the business and its owners in the event of the death of a key employee or family member. It is important to ensure that these policies are in place before the transition takes place.

The transition process should also include the consideration of any taxes and fees that may be applicable. This may include estate taxes, capital gains taxes, and other taxes that may be applicable. It is important to ensure that all of the relevant taxes and fees are paid before the transition takes place.

Finally, the transition process should include the consideration of any other related entities. This may include trustees, executors, or other entities. It is important to ensure that all of the relevant entities are aware of the terms and conditions of the buy-sell agreement and that they agree to the terms.

With proper planning and the help of a business succession planning consultant, business owners can ensure the future of their business and its owners. The transition process should be undertaken with the utmost care and consideration to ensure the business’s future success. With a well-developed succession plan, business owners can ensure the security of their business and its owners for many years to come.

Business Succession Law

Business succession planning is the process in which long-term needs are identified and addressed. The main concern in succession planning is in providing for the continuation of business operations in the event that the owner or manager retires or suddenly becomes incapacitated or deceased. This can occur by several means, such as transferring leadership to the following generation of family members or by naming a specific person to become the next owner. It is highly advantageous to have a business succession plan. Such a plan can create several benefits for the business, including tax breaks and no gaps in business operations. The plan will be formally recorded in a document, which is usually drafted by an attorney. A business succession plan is similar to a contract in that it has binding effect on the parties who sign the document and consent to the plan. Therefore, the main advantage of having a succession plan is that the organization will be much better prepared to handle any unforeseen circumstances in the future.

A well thought out succession plan will be both very broad in scope and specific in detailed instruction. It should include many provisions to address other concerns besides the issue of who will take over ownership.

A business succession plan should include:

• Approximate dates or time frames when succession will begin. For example, the projected date of the owner’s retirement. Instructions should also be composed for steps to take as the date approaches.

• Provisions for what should occur in case of the owner’s unexpected incapacitation, such as in the event of severe illness or death. A replacement should be named in these provisions, and you should state how long their responsibilities will last (i.e., permanent or temporary).

• Identification of who will be the next successor or a guideline for how election should occur, and instructions to ensure a smooth transition.

• A strategic plan for the business after the succession has taken place. This should include any new revisions to current policies and management structures.

As you might expect, there are many legal matters to be addressed when creating a succession plan. Some common issues that arise in connection with business succession include:

• Choice of successor: If the succession plan does not clearly name a successor, it can lead to disputes, especially amongst family members who may be inheriting the business. Be sure to state exactly who will take charge.

• Property distribution: If there is any property in the previous owner’s name, this will need to be addressed so that the property can be distributed upon or during transition.

• Type of business form: Every type of business has different requirements regarding succession. For example, if the business is a corporation, the previous owner’s name must be removed from the articles of incorporation and replaced with that of the successor’s name. On the other hand, partnerships will usually dissolve upon the death of a partner, and it must be re-formed unless specific provisions are made in a contract.

• Tax issues: Any outstanding taxes, debts, or unfinished business must be resolved. Also, if the owner has died, there may be issues with death taxes.

• Benefits: You should ask whether the business will continue to provide benefits even after the owner has retired. For example, health care, life insurance, and retirement pay must be addressed.

• Employment contracts: If there are any ongoing employment contracts, these must be honored so as to avoid an employment law disputes. For example, if there is going to be a change in management structure, it must take into account any provisions contained in the employees’ contracts.

Picking the Successor

When creating the business succession plan, it is crucial that the person that succeeds the current owner is able to continue the company successfully. Without this ability, many individuals may be crossed off the list. Otherwise, it is just easier to sell the organization to someone that the owner has not invested interest in, and the continued transactions and revenue mean nothing personal. One of the primary reasons to have a business succession plan is to ensure the company continues functioning after the owner either enters retirement or dies. For the successor to be a family member, he or she must be fully prepared to work hard and invest time and energy into the business. Many owners of a business have multiple family members or assistants that could take his or her place. It is important to assess both the strengths and weaknesses of each individual so he or she is able to choose the person best suited for the position. There could be resentment and negative emotions that affect the arrangement with other members of the family, and this must be taken into account along with keeping other relationships from becoming complicated such as a spouse or the manager of the business who may have assumed he or she would take on the ownership or full run of the company.

Finalizing the Process

While some may sell the company before retiring or death, it is still important to determine the value of the business before the plan is finalized. This means an appraisal and documentation with the successor’s name and information. Additional items may need to be purchased such as life insurance, liability coverage and various files with the transfer of ownership if the owner is ready to conclude the proceedings. The current owner may also be provided monetary compensation for his or her interest or a monthly stipend based on the profits of the company. These matters are determined by the paperwork and possession of the business. The transfer may be possible through a cross-purchase agreement where each party has a policy on the partners in the business. Each person is both owner and beneficiary simultaneously. This permits a buyout of shares or interest when one partner dies if necessary. An entity purchase occurs with the policy being both beneficiary and owner. Then the shares are transferred to the company upon the death of one person. Succession plans are commonly associated with retirement; however, they serve an important function earlier in the business lifespan: If anything unexpected happens to you or a co-owner, a succession plan can help reduce headaches, drama, and monetary loss. As the complexity of the business and the number of people impacted by the exit grows, so does the need for a well-written succession plan.

You should consider creating successions plan if you:

• Have complex processes: How will your employees and successor know how to operate the business once you exit? How will you duplicate your subject matter expertise?

• Employ more than just yourself: Who will step in to lead employees, administer human resources (HR) and payroll, and choose a successor and leadership structure?

• Have repeat clients and ongoing contracts: Where will clients go after your exit, and who will maintain relationships and deliver on long-term contracts?

• Have a successor in mind: How did you arrive at this decision, and are they aware and willing to take ownership?

When to Create a Small Business Succession Plan

Every business needs a succession plan to ensure that operations continue, and clients don’t experience a disruption in service. If you don’t already have a succession plan in place for your small business, this is something you should put together as soon as possible. While you may not plan to leave your business, unplanned exits do happen. In general, the closer a business owner gets to retirement age, the more urgent the need for a plan. Business owners should write a succession plan when a transfer of ownership is in sight, including when they intend to list their business for sale, retire, or transfer ownership of the business. This will ensure the business operates smoothly throughout the transition. There are several scenarios in which a business can change ownership. The type of succession plan you create may depend on a specific scenario. You may also wish to create a succession plan that addresses the unexpected, such as illness, accident, or death, in which case you should consider whether to include more than one potential successor.

Selling Your Business to a Co-owner

If you founded your business with a partner or partners, you may be considering your co-owners as potential successors. Many partnerships draft a mutual agreement that, in the event of one owner’s untimely death or disability, the remaining owners will agree to purchase their business interests from their next of kin. This type of agreement can help ease the burden of an unexpected transition—for the business and family members alike. A spouse might be interested in keeping their shares but may not have the time investment or experience to help it blossom. A buy-sell agreement ensures they’re given fair compensation, and allows the remaining co-owners to maintain control of the business.

Passing Your Business Onto an Heir

Choosing an heir as your successor is a popular option for business owners, especially those with children or family members working in their organization. It is regarded as an attractive option for providing for your family by handing them the reins to a successful, fully operational enterprise. Passing your business on to an heir is not without its complications. Some steps you can take to pass your business onto an heir smoothly are:

• Determine who will take over: This is an easy decision if you already have a single-family member involved in the business but gets more complicated when multiple family members are interested in taking over.

• Provide clear instructions: Include instructions on who will take over and how other heirs will be compensated.

• Consider a buy-sell agreement: Many succession plans include a buy-sell agreement that allows heirs that are not active in the business to sell their shares to those who are.

• Determine future leadership structure: In businesses where many heirs are involved, and only one will take over, you can simplify future discussions by providing clear instructions on how the structure should look moving forward.

Selling Your Business to a Key Employee

When you don’t have a co-owner or family member to entrust with your business, a key employee might be the right successor. Consider employees who are experienced, business-savvy, and respected by your staff, which can ease the transition. Your org chart can help with this. If you’re concerned about maintaining quality after your departure, a key employee is generally more reliable than an outside buyer. Just like selling to a co-owner, a key employee succession plan requires a buy-sell agreement. Your employee will agree to purchase your business at a predetermined retirement date, or in the event of death, disability, or other circumstance that renders you unable to manage the business.

Selling Your Business to an Outside Party

When there isn’t an obvious successor to take over, business owners may look to the community: Is there another entrepreneur, or even a competitor, that would purchase your business? To ensure that the business is sold for the proper amount, you will want to calculate the business value properly, and that the valuation is updated frequently. This is easier for some types of businesses than others. If you own a more turnkey operation, like a restaurant with a good general manager, your task is simply to demonstrate that it’s a good investment. They won’t have to get their hands dirty unless they want to and will ideally still have time to focus on their other business interests. Meanwhile, if you own a real estate company that’s branded under your own name, selling could potentially be more challenging. Buyers will recognize the need to rebrand and remarket and, as a result, may not be willing to pay full price. Instead, you should prepare your business for sale well in advance; hire and train a great general manager, formalize your operating procedures, and get all your finances in check. Make your business as stable and turnkey as possible, so it’s more attractive and valuable to outside buyers.

Selling Your Shares Back to the Company

The fifth option is available to businesses with multiple owners. An “entity purchase plan” or a “stock redemption plan” is an arrangement where the business purchases life insurance on each of the co-owners. When one owner dies, the business uses the life insurance proceeds to purchase the business interest from the deceased owner’s estate, thus giving each surviving owners a larger share of the business.

Reasons to Hire a Business Succession Attorney

• Decisions during the Idea Stage: Even before you officially open your doors for business, you have several decisions to make that will affect your daily operations going forward. What will you call your company? Is the name you have in mind available? What is your marketing tag line? Can you use that without encountering any problems? Where will your business be located? Are there any zoning issues of which you need to be aware? These are just a few examples of decisions that need to be made before you even start doing what it is you want to do. These decisions will be a lot easier to make with the help of a business attorney.

• Startup Protocols and Legal Requirements: Another early decision you’re going to have to make involves the specific type of business entity you want to initiate. You need to do so for several reasons, not the least of which is that most types of business entities require some sort of registration and all businesses will need to register and obtain a business license from the local municipalities in which they operate. In addition, you may need to provide public notice of the intention of starting a business entity, which could involve publishing that notice in a newspaper for four weeks. You need to do this right or you could face other problems, which is another reason why hiring a lawyer for your business startup is a wise decision.

• Banking Questions: If you’re going to start a business, you’re also going to need to open a bank account or perhaps multiple bank accounts. You may also need to apply for credit in the forms of credit cards and/or lines of credit if attainable. It’s highly advisable for a plethora of reasons to keep all of your business finances completely separate from your personal situation, as it’ll be much easier to organize those separate forms of finances come tax time or should any other questions arise. A small business attorney can help you choose the proper bank and the type of account or accounts you should look to open so you don’t wind up scrambling after you begin your core mission.

• Tax Questions: Since the founding of our country, a common quote that people tend to repeat in several contexts is, “Nothing is certain except for death and taxes.” What is not debatable is that your business will be taxed in one way or another, and you need a lawyer for your business startup to make sure that you’re both in compliance with local, state and federal tax codes and so that you’re not unnecessarily facing double taxes. Tax questions should be answered before you get started so you know what to generally expect in this regard, and from there you should work with a tax accountant for your specific tax questions.

• Insurance Questions: One of the issues that you’ll begin to hear and think more about as you get ready to start your business involves liability. You are responsible for the product or service you provide to your clients or customers, and you want to make sure that you’re protected from personal liability should something go wrong. You may also need to comply with regulations that require some sort of liability insurance coverage, but choosing the proper coverage and understanding the nature of that coverage are involved tasks that need to be done right. A small business attorney can help guide your business towards the coverage you need while simultaneously helping you minimize the chance for unexpected and unpleasant surprises down the road.

• Debt Management: For most Americans, debt is simply a part of life. For the majority of small business owners, debt is something that exists even before they open their doors. Debt is real and it doesn’t go away easily, and like anything else, questions, confusion and problems relating to debt can arise that can harm your ability to push your organization forward. The best way to manage debt issues is by way of advice from a business attorney who can explain the legalities involved with it and fight for you if there is a problem.

• Dispute Advocacy: It’s common for any business to encounter disputes of one type or another. It’s also unfortunately common for a startup business to wind up dealing with a problem with a vendor or some larger, more established entity. Regardless, owners need a small business attorney at the ready to fight for their company when such situations arise. An attorney who isn’t going to hesitate to advocate zealously for clients can level the playing field and even help resolve issues before they become much larger problems. In some cases, even mentioning that you have an attorney representing you could help avoid those problems altogether.

Business Succession Lawyer Lehi Utah Consultation

When you need legal help with a business succession in Lehi Utah, call Jeremy D. Eveland, MBA, JD (801) 613-1472.

Jeremy Eveland

17 North State Street

Lindon UT 84042

(801) 613-1472

For legal assistance regarding Business Succession Lawyer Lehi Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Lehi Utah cases and provide guidance on Business Succession Lawyer Lehi Utah for clients.

For legal assistance regarding Business Succession Lawyer Lehi Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Lehi Utah cases and provide guidance on Business Succession Lawyer Lehi Utah for clients.

For legal assistance regarding Business Succession Lawyer Lehi Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Lehi Utah cases and provide guidance on Business Succession Lawyer Lehi Utah for clients.

For legal assistance regarding Business Succession Lawyer Lehi Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Lehi Utah cases and provide guidance on Business Succession Lawyer Lehi Utah for clients.

For legal assistance regarding Business Succession Lawyer Lehi Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Lehi Utah cases and provide guidance on Business Succession Lawyer Lehi Utah for clients.

For legal assistance regarding Business Succession Lawyer Lehi Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Lehi Utah cases and provide guidance on Business Succession Lawyer Lehi Utah for clients.

For legal assistance regarding Business Succession Lawyer Lehi Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Lehi Utah cases and provide guidance on Business Succession Lawyer Lehi Utah for clients.

For legal assistance regarding Business Succession Lawyer Lehi Utah, contact Jeremy Eveland. We handle Business Succession Lawyer Lehi Utah cases and provide guidance on Business Succession Lawyer Lehi Utah for clients.

If you are ready to speak with a corporate lawyer fill in the contact form below and we will reach out to you and schedule a consultation:

A corporate lawyer or corporate counsel is a type of lawyer who specializes in corporate law. Corporate lawyers working inside and for corporations are called in-house counsel. The corporate lawyer performs multiple essential functions in a corporation. Among the functions of a corporate lawyer are to ensure corporate housekeeping, review and evaluate contracts and legal documents, provide advisory support to the corporation’s executive leadership, and render their opinions and interpretations of pertinent court rulings. Corporate lawyers also guide corporate governance, ensure regulatory compliance, and manage due diligence.

A company or corporation is a complex organization that consists of multiple business, legal and financial concepts, devices, and relationships all rolled into one. The corporation, for example, is an agreement by the founders and the shareholders to set up a legal entity that will conduct their business operations. The corporation is also the employer of its worker, as well as the recipient of investors’ money.

Roles and Responsibilities of a Corporate Lawyer

The role of a corporate lawyer is to ensure the legality of commercial transactions, advising corporations on their legal rights and duties, including the duties and responsibilities of corporate officers. In order for them to do this, they must have knowledge of aspects of contract law, tax law, accounting, securities law, bankruptcy, intellectual property rights, licensing, zoning laws, and the laws specific to the business of the corporations that they work for. In recent years, controversies involving well-known companies around have highlighted the complex role of corporate lawyers in internal investigations, in which attorney client privilege could be considered to shelter potential wrong doing by the company. If a corporate lawyer’s internal company clients are not assured of confidentiality, they will be less likely to seek legal advice, but keeping confidences can shelter society’s access to vital information.

The practice of corporate law Is less adversarial than that of trial law or other areas or aspects of law. Lawyers for both sides of a commercial transaction are less opponents than facilitators. One lawyer, is mostly characterized then as “the handmaidens of the deal”. Transactions take place amongst peers. There are rarely wronged parties, underdogs, or inequities in the financial means of the participants. Corporate lawyers structure those transactions, draft documents, review agreements, negotiate deals, and attend meetings.

The areas of corporate law a corporate lawyer experiences depend from the geographic location of the lawyer’s law firm and the number of lawyers in the firm and the types of corporations they deal or work with. A small town corporate lawyer in a small firm may deal in many short-term jobs such as drafting wills, divorce settlements, and real estate transactions, whereas a corporate lawyer in a large city firm may spend many months devoted to negotiating a single business transaction for a single client or corporation. Similarly, different firms may organize their subdivisions in different ways. Not all will include mergers and acquisitions under the umbrella of a corporate law division, for example.

Some corporate lawyers become partners in their firms. Others become in-house counsel for corporations while others may migrate to other professions such as investment banking and teaching law.

What Does A Corporate Lawyer Actually Do?

What do you picture when you hear the term “Corporate lawyer?” Is it a man or woman in a nice suit, carrying a briefcase, walking swiftly up the stairs of a stately government building? While many of us are able to conjure up an image of what we think a corporate lawyer looks like, not many of us can (accurately and correctly) imagine what a corporate lawyer actually does all day.

What Is the Role of a Corporate Lawyer?

The role of a corporate lawyer is to advise clients of their rights, responsibilities, and duties under the law. When a corporate lawyer is hired by a corporation, the lawyer represents the corporate entity, not its shareholders or employees. This may be a confusing concept to grasp until you learn that a corporation is actually treated a lot like a person under the law.

A corporation is a legal entity that is created under state law, usually for the purpose of conducting business. A corporation is treated as a unique entity or “as a person” under the law, separate from its owners or shareholders. Corporate law includes all of the legal issues that surround a corporation, which are many because corporations are subject to complex state and federal regulations. Most states require corporations to hold regular meetings, such as annual shareholder meetings, along with other requirements. Corporate lawyers make sure corporations are in compliance with these rules, while taking on other types of work.

What Type of Work Do Corporate Lawyers Do?

Contrary to popular belief, most corporate lawyers rarely step foot in courtrooms while some never has and probably never will. Instead, most of the work they do is considered “transactional” in nature. That means they spend most of their time helping a corporation to avoid litigation.

More specifically, corporate lawyers may spend their time working on:

Contracts: Reviewing, drafting, and negotiating legally-binding agreements on behalf of the corporation, which could involve everything from lease agreements to multi-billion dollar acquisitions

Mergers and acquisitions (M&A): Conducting due diligence, negotiating, drafting, and generally overseeing “deals” that involve a corporation “merging” with another company or “acquiring” (purchasing) another company

Corporate governance: Helping clients create the framework for how a firm is directed and controlled, such as by drafting articles of incorporation, creating bylaws, advising corporate directors and officers on their rights and responsibilities, and other policies used to manage the company

Venture capital: Helping startup or existing corporations find capital to build or expand the business, which can involve either private or public financing

Securities: Advising clients on securities law compliance, which involves the complex regulations aimed at preventing fraud, insider training, and market manipulation, as well as promoting transparency, within publicly-traded companies

In many cases, corporate lawyers work in large or mid-size law firms that have corporate law departments. Many corporate lawyers have specialties or areas of corporate law that they focus on such as M&A, venture capital, or securities. Some corporate lawyers work in-house, and most large corporations have their own in-house legal departments. In-house corporate lawyers generally handle a wide variety of issues.

What Does Someone Need to Do to Become a Corporate Lawyer?

The path to becoming a corporate lawyer is not that different from the path to practicing another area of law. To become a corporate lawyer, one needs to attend law school to obtain a juris doctor (J.D.) degree and be licensed to practice law in their state. Oftentimes, corporate lawyers have past work experience in business, but this is generally not required.

What Skills Do Corporate Lawyers Need?

Corporate lawyers should have excellent writing, communication, and negotiating skills because these skills are relied upon so heavily in day-to-day corporate law work.

Because corporate law is a diverse practice area that touches on many different transnational, regulatory, and business-related matters, it’s important for a corporate lawyer to have the desire to learn about many different areas of law, unless they want to specialize in one niche area such as securities law.

Additionally, many corporate lawyers have multiple clients in different industries, which means they must be willing to learn the ins and outs of those unique industries they get involved with.

Finally, corporate lawyers need the skills and wherewithal to reach out to other lawyers when they reach a specialized topic that they don’t have experience with such as tax, ERISA, employment, or real estate.

Utah Corporate Lawyer

Jeremy Eveland is an experienced corporate lawyer and a highly-sought after attorney in the corporate legal field. He has a strong background in corporate law and has been practicing for awhile, making him a valuable asset to any company or law firm looking for a corporate lawyer.

Jeremy has a Bachelor of Arts degree from Brigham Young University. He does not have Bachelor of Science degree in Business Administration from the University of California, Los Angeles. Jeremy has a Juris Doctorate degree from Gonzaga University Law School in Spokane Washington, which he obtained in 2003 and was awarded the designation cum laude, which means with praise or with honors. He did not receive a Juris Doctor degree from the University of California, Berkeley’s School of Law. Jeremy is a member of the Utah Bar Association. He is not a member of the New York State Bar Association. Jeremy currently serves as an general counsel for a large corporation and has some other business and corporate clients.

Jeremy’s experience in corporate law and the legal profession is immense. He has represented clients in a variety of corporate transactions, such as mergers and acquisitions, intellectual property, and civil litigation. Additionally, Jeremy has also worked on legal matters pertaining to small businesses, large corporations, and governmental entities. He is well-versed in all relevant corporate laws, including those pertaining to taxes, finance, regulations, and employees. He also has an understanding of corporate law regarding issues such as insurance, trademarks, copyrights, and intellectual property.

Jeremy is a corporate attorney and has worked for a few different law firms over the years. He has worked on civil law issues, criminal law matters, and corporate law matters in both state and federal courts. He also clerked for Supreme Court Justice Mark Gibbons and has provided legal counsel to many other businesses.

The work of a corporate lawyer requires many skills and experience. Jeremy has the necessary qualifications and experience to succeed as a corporate lawyer. He is a good communicator and is able to effectively explain complex legal matters to clients and colleagues. He is also knowledgeable in many areas of corporate law, including finance, regulations, taxes, and insurance. In addition, Jeremy is highly organized and has a strong attention to detail, which makes him a great asset to any corporate law firm or organization.

In addition to his excellent legal skills, Jeremy also has a strong understanding of corporate law and the business world. Jeremy has a master of business administration degree and has worked with international businesses on issues of supply, demand, and labor. He is able to provide legal advice to corporate clients on a variety of issues, including corporate transactions, mergers and acquisitions, and legal matters pertaining to intellectual property. He also has a keen understanding of the regulations and laws that govern the corporate world.

For any company or law firm looking for a corporate lawyer, Jeremy Eveland is an excellent choice. He has the skills, experience, and qualifications necessary to excel in the field of corporate law. He has the knowledge and experience to handle any legal matter, ranging from small businesses to mid-zise businesses, in the multi-million dollar range to even large global corporations. His experience in corporate law and the legal profession make him a valued asset to any organization or law firm.

For any company or law firm looking for a corporate lawyer, Jeremy Eveland is the perfect person for the job. His experience, qualifications, and skills make him an ideal candidate for the job. He is an excellent communicator, has a strong understanding of corporate law, and is highly organized. With his strong background in corporate law, he is a valuable asset to any organization. He is a great choice for any company or law firm looking for an outside corporate lawyer.

When Might an Individual or Business Need Help From a Corporate Lawyer?

A corporate lawyer advises firms on how to comply with rules and laws, but that’s only the beginning. In truth, any individual starting a business venture could benefit from a corporate lawyer. Why? Because a corporate lawyer can help you structure and plan your business for success, even if you end up going with a business structure other than a corporation. It’s always a good Idea to have a lawyer on board to craft your business’ managing documents, review contracts, and help you make other strategy decisions.

Of course, it’s not always possible for smaller businesses (or even medium-sized businesses) to have a corporate lawyer on retainer, but one should be consulted when forming a business, when closing a business, and when problems arise, at the very least.

Consider meeting with a corporate lawyer in your area if you are starting a business venture or need advice on anything else related to business transactions or planning.

Corporate Lawyer at Work in the Office

The corporate lawyer has to make sure all these legal aspects of a corporation’s existence are adequately managed and serviced. The corporate lawyer performs a lot of roles and functions. If you have a growing enterprise or you are an executive officer of a large corporation operating out of Utah, you might have to consider discussing your company’s issues and concerns with some Corporate Lawyers.

Utah Corporate Attorney Consultation

When you need legal help with a corporate law in Utah, call Jeremy D. Eveland, MBA, JD (801) 613-1472.

Jeremy Eveland

17 North State Street

Lindon UT 84042

(801) 613-1472

What Is Business Law and How Does It Affect Your Business?

Last Updated: June 11, 2026

Business law in Utah is a body of law that governs the formation, operation, and dissolution of businesses in the state of Utah. This legal field encompasses a wide range of topics, including contract law, corporate law, and labor law. Utah business law also covers a variety of other areas, such as business licensing and taxation. This article will explore the history of business law in Utah, the various types of law related to business in Utah, and the impact of business law on businesses located in the state.

History of Business Law in Utah

Business law in Utah has evolved over time, as the state has adapted to changing economic conditions and technological developments. Initially, the state’s legal framework was largely based on the English common law system. This system was adopted by the state’s original settlers, who were largely of English origin. Over time, the state developed its own set of business laws that incorporated elements of the English common law system.

Utah’s business laws were further developed in the late 19th century, when the state experienced a period of industrial growth. This period saw the passage of various laws that sought to provide protection for businesses, such as the formation of limited liability companies and the adoption of the Uniform Commercial Code (UCC). These laws remained largely unchanged until the mid-20th century, when the state began to recognize the importance of technology in the business world and began to pass laws that addressed the various issues that technology can create.

Types of Business Law in Utah

Business law in Utah covers a wide range of topics, including contract law, corporate law, labor law, and business licensing and finally business taxation. Bankruptcy law, Federal law and other laws can play a role for your business as well. For example, if you have a construction business, you’ll need a contractor’s license or if you’re a dentist, you’ll need a dental license, etc.

Contract Law

Contract law in Utah is governed by the state’s version of the UCC, which was adopted in 1973. This law governs the formation, performance, and termination of contracts between individuals and businesses. It also sets out the remedies that may be available in the event of a breach of contract. Contract law is an important part of the legal system in the state of Utah. It provides the framework for the enforcement of agreements between parties. This article has explored the various aspects of contract law in Utah, as well as the requirements for the formation and enforcement of contracts in the state. Additionally, this article has discussed the remedies available to parties in the event of a breach of contract.

Corporate Law

Corporate law in Utah is largely based on the state’s version of the Model Business Corporation Act (MBCA). This is codified as Utah Code 16-10a. This law governs the formation, operation, and dissolution of corporations in the state. It sets out the rights and obligations of corporate shareholders, directors, and officers, as well as the procedures for issuing shares and holding shareholder meetings.

Utah corporate laws are among some of the most well established in the nation. Companies that are established in Utah must adhere to the rules and regulations set forth by the state. These laws govern all aspects of running a business, from the capital structure to the fiduciary responsibilities of directors and shareholders. The Utah Business Corporation Act governs the formation and operation of corporations in the state, and outlines the rules for issuing shares and preferred stock, paying dividends, and winding up the company if necessary.

Under Utah corporate laws, a liquidator is appointed when a company is winding up and is responsible for settling the company’s debts and distributing assets. In the event of compulsory liquidation, the court appoints a liquidator who is responsible for overseeing the process. The liquidator also has the power to sue for the recovery of assets, and to bring legal action against anyone who has been found to be in breach of the company’s fiduciary duties.

Under Utah corporate laws, directors and shareholders are obligated to disclose any material non-public information, such as insider trading, they may have. Any breach of these obligations can result in a lawsuit. Furthermore, the capital structure of the company must adhere to the rules outlined in the Utah Business Corporation Act. This includes the payment of preferred dividends and the issuance of preference shares.

Utah corporate laws are studied extensively in law school, and the Law School Admission Test (LSAT) includes a section devoted to corporate law. Many Utah law schools have professors who specialize in corporate law, and those wishing to practice corporate law in Utah must have a thorough understanding of the state’s laws.

Labor Law

Labor law in Utah is governed by the state’s labor code, which sets out the rights and responsibilities of employers and employees. It is codified as Utah Code 34A-1-101 et seq. It also establishes minimum wage and overtime pay requirements, as well as workplace safety standards.

Business Licensing and Taxation

Businesses operating in Utah must obtain a business license from the state. The state also imposes various taxes on businesses, such as income tax, sales tax, and property tax.

Impact of Business Law in Utah on Businesses

Every business in Utah is affected by business laws. Business law in Utah has a significant impact on businesses operating in the state. The various laws related to business in Utah provide legal protection for businesses and ensure that they are able to operate in a safe and fair environment. The laws also provide guidance on how businesses should conduct themselves and help to ensure that businesses comply with all applicable laws and regulations.

Business law in Utah is governed by both state and federal laws. The state of Utah has its own laws and regulations that need to be followed by businesses operating in the state. Federal laws are also enforced in Utah, such as the Sherman Act and the Clayton Act, which are antitrust statutes that prohibit monopolies, price-fixing, and other trade practices that are considered anti-competitive.

The Fair Labor Standards Act (FLSA) is a federal law that sets standards for overtime pay, minimum wage, and other labor related issues. Businesses in Utah must adhere to the provisions of the FLSA, as well as the state of Utah’s own labor and employment laws.

The Federal Trade Commission (FTC) is responsible for enforcing antitrust statutes in the state of Utah. The FTC is charged with investigating and punishing companies that engage in colluding and other anti-competitive practices. The FTC also enforces the law against deceptive and misleading advertising.

Businesses in the Mountain West and Southwest regions of the United States and all along with Wasatch Front must be aware of the laws and regulations governing tip pools and tip sharing, as well as the requirements for registering an agent for service of process.

Any businesses operating in the state of Utah need to be aware of the federal and state laws governing their operations, including those related to antitrust, labor and employment, advertising, and registration of an agent for service of process. Failing to comply with these laws can result in heavy fines and other penalties.

Consultation With A Utah Business Lawyer

Business law in Utah is an important area of law that governs the formation, operation, and dissolution of businesses in the state. The various types of business law in Utah, such as contract law, corporate law, labor law, and business licensing and taxation, all play an important role in ensuring that businesses in the state are able to operate in a legal and fair environment. Business law in Utah also has a significant impact on businesses by providing them with legal protection and guidance on how to properly conduct their operations.

Utah Business Lawyer Free Consultation

When you need a Utah business attorney, call Jeremy D. Eveland, MBA, JD (801) 613-1472.

Jeremy Eveland

17 North State Street

Lindon UT 84042

(801) 613-1472

Salt Lake City (often shortened to Salt Lake and abbreviated as SLC) is the capital and most populous city of Utah, as well as the seat of Salt Lake County, the most populous county in Utah. With a population of 200,133 in 2020,[10] the city is the core of the Salt Lake City metropolitan area, which had a population of 1,257,936 at the 2020 census. Salt Lake City is further situated within a larger metropolis known as the Salt Lake City–Ogden–Provo Combined Statistical Area, a corridor of contiguous urban and suburban development stretched along a 120-mile (190 km) segment of the Wasatch Front, comprising a population of 2,606,548 (as of 2018 estimates),[11] making it the 22nd largest in the nation. It is also the central core of the larger of only two major urban areas located within the Great Basin (the other being Reno, Nevada).

Salt Lake City was founded July 24, 1847, by early pioneer settlers, led by Brigham Young, who were seeking to escape persecution they had experienced while living farther east. The Mormon pioneers, as they would come to be known, entered a semi-arid valley and immediately began planning and building an extensive irrigation network which could feed the population and foster future growth. Salt Lake City’s street grid system is based on a standard compass grid plan, with the southeast corner of Temple Square (the area containing the Salt Lake Temple in downtown Salt Lake City) serving as the origin of the Salt Lake meridian. Owing to its proximity to the Great Salt Lake, the city was originally named Great Salt Lake City. In 1868, the word “Great” was dropped from the city’s name.[12]

Salt Lake City has developed a strong tourist industry based primarily on skiing and outdoor recreation. It hosted the 2002 Winter Olympics. It is known for its politically progressive and diverse culture, which stands at contrast with the rest of the state’s conservative leanings.[13] It is home to a significant LGBT community and hosts the annual Utah Pride Festival.[14] It is the industrial banking center of the United States.[15] Salt Lake City and the surrounding area are also the location of several institutions of higher education including the state’s flagship research school, the University of Utah. Sustained drought in Utah has more recently strained Salt Lake City’s water security and caused the Great Salt Lake level drop to record low levels,[16][17] and impacting the state’s economy, of which the Wasatch Front area anchored by Salt Lake City constitutes 80%.[18]

For legal assistance regarding How Does It Affect, contact Jeremy Eveland. We handle How Does It Affect cases and provide guidance on How Does It Affect for clients.

For legal assistance regarding How Does It Affect, contact Jeremy Eveland. We handle How Does It Affect cases and provide guidance on How Does It Affect for clients.

For legal assistance regarding How Does It Affect, contact Jeremy Eveland. We handle How Does It Affect cases and provide guidance on How Does It Affect for clients.

For legal assistance regarding How Does It Affect, contact Jeremy Eveland. We handle How Does It Affect cases and provide guidance on How Does It Affect for clients.

For legal assistance regarding How Does It Affect, contact Jeremy Eveland. We handle How Does It Affect cases and provide guidance on How Does It Affect for clients.

For legal assistance regarding How Does It Affect, contact Jeremy Eveland. We handle How Does It Affect cases and provide guidance on How Does It Affect for clients.

For legal assistance regarding How Does It Affect, contact Jeremy Eveland. We handle How Does It Affect cases and provide guidance on How Does It Affect for clients.

For legal assistance regarding How Does It Affect, contact Jeremy Eveland. We handle How Does It Affect cases and provide guidance on How Does It Affect for clients.

This Estate Planning post will attempt to tell you what you need to know about estate planning. Obviously it is hard to provide all information about every aspect of estate planning in one post, but we will touch upon each of the essential elements. Also, if you have questions about estate planning in Utah, call Jeremy Eveland for a free consultation (801) 613-1472.

Estate planning is an important part of life, no matter which state you live in. In Utah, estate planning is the process of planning for the management of someone’s assets, property, and other possessions after their death. It is important to understand the basics of estate planning so that you can make the best decisions for yourself and your family.

What is Estate Planning in Utah?

Estate planning in Utah is the process of creating documents and other measures to ensure that your wishes are carried out after your death. This includes creating a will, trust, power of attorney, and health care directive to ensure that your assets, property, and other possessions are passed on according to your wishes. Estate planning also involves making decisions about taxes on your estate, who will be the executor of your estate, and who will make medical decisions for you if you are unable to do so yourself.

Why Get a Complete Estate Plan Done?

Creating a comprehensive estate plan is important because it will provide your loved ones with the peace of mind that your wishes will be carried out after you pass away. It will also protect your assets and property, allowing them to be passed on to your beneficiaries with minimal tax or other costs. Additionally, it will provide your family with the guidance they need to make decisions about how to handle your estate in the event of your death.

Why Does an Estate Plan Use a Will, Trust, Power of Attorney and Health Care Directive?

A will is a legal document that outlines how you want your assets and property to be distributed after you pass away. It can also appoint an executor to carry out your wishes and make sure that your legacy is carried out according to your wishes. A trust is a legal document that allows you to transfer your assets and property to a third party, such as a family member or a charity, while you are still alive. This can help reduce estate taxes, and can also help you protect your assets and property.

A power of attorney is a document that allows you to appoint someone to make financial and legal decisions on your behalf if you are unable to do so yourself. A health care directive is a document that outlines your wishes regarding medical care should you become incapacitated and unable to make decisions for yourself.

Durable Power of Attorney

Durable Power of Attorney in Utah is an important document when it comes to estate planning. It is a legal document that allows someone to act on behalf of the principal when it comes to managing their financial and medical decisions. This document is especially important for those who are unable to make decisions for themselves due to age, disability, or illness.

When it comes to estate planning in Utah, there are several important tasks that need to be completed. These include creating a trust, setting up beneficiary designations for accounts, and determining who will be the executor of the estate. In addition, there are also important tax considerations that must be taken into account. A CFP® professional can help individuals understand the tax implications of their estate plan.

When it comes to the durable power of attorney, it is important to understand the different types that exist. These include financial power of attorney, health care power of attorney, and guardianship. The American Bar Association recommends that individuals create a durable power of attorney as part of their estate plan. This document will allow someone to make decisions on behalf of the principal in the event that they are unable to do so.

Creating a durable power of attorney in Utah can be a complicated process. It is important to consult with an estate planning attorney to ensure that the document is properly drafted and all of the necessary tasks are completed. There are also helpful guides and estate planning checklists that can be used to ensure that everything is taken care of properly.

In addition to creating a durable power of attorney in Utah, it is also important to create other documents such as a living trust, last testament, and life insurance policy. These documents can help ensure that assets are managed according to the wishes of the principal, and that the heirs and beneficiaries of the estate are taken care of.

Estate planning in Utah is an important process, and one that should not be taken lightly. It is important to consult with a trusted financial advisor, estate planning attorney, or estate planner to ensure that the estate plan is created properly and that all of the necessary documents are drafted. With the help of these professionals, individuals can create a plan that is tailored to their needs and that will provide peace of mind to their loved ones.

Health Care Directive

Making a health care directive in Utah can be a complex process, and it’s important to have all the necessary documents in place to ensure your wishes will be honored in the event of your incapacity. Estate planning involves a variety of documents, including wills, trusts, power of attorneys, and life insurance policies, all of which can be used to protect your assets, care for your family, and make sure your beneficiaries are taken care of when you’re gone.

Estate planning begins with a thorough review of your assets and liabilities. An estate-planning attorney can help you determine the best way to organize your assets and minimize the impact of federal and state taxes. You will also need to decide how to distribute your property and assets among your beneficiaries, and how to allocate your estate taxes.

Once you have a plan in place, you will need to create the legal documents that will ensure your wishes are carried out. Your estate plan should include a will, a trust, and a durable power of attorney. A will is used to specify who will receive your property and assets when you pass away, and a trust can be used to manage and protect your assets during your lifetime. A durable power of attorney will give someone else the power to make decisions on your behalf if you become incapacitated.

In addition to these documents, you may need to create other documents to protect your loved ones. Beneficiary designations, for example, can be used to ensure that your life insurance benefits are paid to the people you choose. It’s also important to review your financial accounts and beneficiary designations on a regular basis to make sure they are up-to-date.

Finally, you may want to create a living will to make sure your wishes are respected in the event of your death. This document can be used to specify your wishes regarding medical care and end-of-life decisions. You may also want to consider creating a guardianship for any minor children you have, or a power of attorney for someone you trust to manage your finances if you become incapacitated.

A health care directive in Utah can help protect your family, your estate, and your assets. Working with a CFP® professional or an estate planner can help ensure your plan is tailored to your specific needs and goals. Estate planning is an important part of taking care of yourself and your loved ones, so it’s a good idea to take the time to create a plan that meets your needs.

Why Does a Business Owner Need Estate Planning?

Estate planning is important for business owners, as it allows them to ensure that their business will continue to be successful after their death. Estate planning for a business involves setting up a trust or other legal structure to ensure that the business is passed on according to your wishes. It also involves making decisions about taxes, beneficiaries, and accounts. Additionally, it involves making sure that the business is structured in a way that will minimize tax costs and maximize the value of the business for future generations.